by Luke Hardacre, push.

Spend time watching how people actually buy bikes online and the pattern is hard to miss.

They do not arrive, click, and buy.

They search, open multiple tabs, move between retailers, check availability, look for reassurance, leave, come back later, and often repeat the process several times before committing. Sometimes the decision finishes online. Sometimes it finishes on the phone or in-store. Often the website is revisited more than once before anything happens.

That behaviour shows up clearly when you look at ecommerce data across UK bike retailers.

Where this data comes from, and why it matters

The patterns described here are not drawn from surveys or opinion.

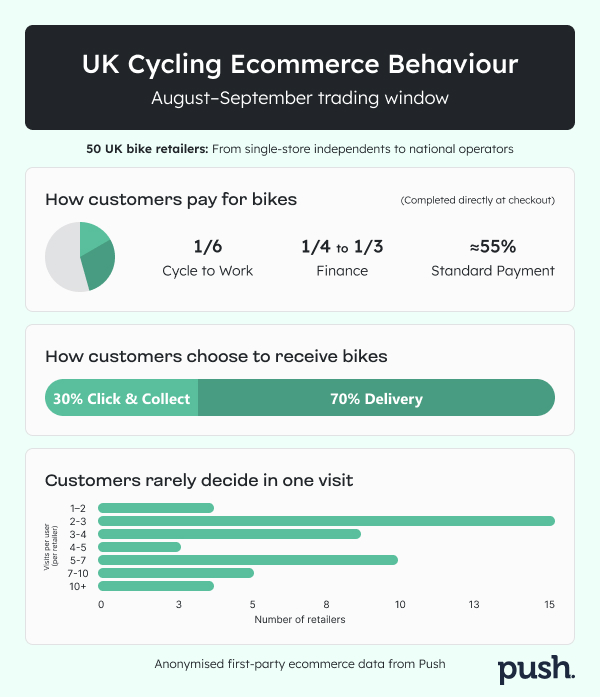

They come from anonymised ecommerce data across a wide range of established UK bike retailers trading on Push. The dataset covers a consistent late-summer trading window (August to September) and includes single-store independents, multi-store groups, and brand-led retailers.

Push exists solely in cycling. It does not power general retail. It does not aggregate across unrelated sectors. Every site in this dataset sells bikes, parts, accessories, or ebikes as a core part of their business.

That focus matters, because customer behaviour in bike retail does not mirror generic ecommerce. The purchase is higher value, more considered, and more trust-dependent. Looking at this data in isolation, within cycling, makes the patterns harder to ignore.

This is not about individual performance. It is about how customers actually behave when choosing where to buy a bike.

In that context, conversion rate stops behaving like a simple measure of website performance. Instead, it increasingly reflects something more fundamental: whether the customer feels confident giving their money to that retailer.

Not whether the site works. Whether the retailer feels trustworthy.

The real question customers are asking

Most customers can find the bike. They can find the price. In many cases they can find the same model listed by several retailers at near-identical pricing.

The harder question is not “can I buy this here?”

It is “should I buy it from these people?”

That judgement is made quickly and often subconsciously. Customers are asking themselves:

- Do these people look established?

- Do they feel reachable if something goes wrong?

- Do I recognise them, or do they look like a retailer I can rely on?

- Do I understand what happens next if I commit?

Retailers know the answers internally. Customers do not. They only experience what the site signals to them, plus whatever prior awareness they already carry.

Conversion rate is where that judgement becomes visible.

Three ways customers tend to perceive bike retailers

Across the dataset, retailers consistently cluster into three customer-perceived groups. This has little to do with store count or turnover, and everything to do with how the retailer is interpreted when a customer lands on the site without context.

Destination retailers with pre-existing trust

Some retailers benefit from recognition before the customer even starts browsing. That trust might come from scale, geography, longevity, brand association, or category authority.

Customers arrive already inclined to believe the retailer is legitimate. The website’s role is confirmation rather than persuasion. Browsing still happens, but it is calmer and more purposeful. Returning visits are common, but they tend to lead somewhere.

In this group, conversion rates are typically stronger because the site is not fighting to establish credibility from scratch.

Price-led or convenience-led retailers

These retailers attract customers who are actively comparing. The draw is availability, speed, or price competitiveness. Shoppers here are often highly sensitive to small differences and quick to move elsewhere.

In the data, this group frequently shows high unique visitor volumes paired with lower-than-expected conversion. That is not a traffic problem. It reflects how these customers behave. They are shopping around, withholding commitment, and looking for reasons not to buy as much as reasons to buy.

Revenue can still be meaningful, but conversion stays pressured because trust is thinner and competition is always visible.

Store-first retailers using ecommerce as a shop window

For many independents, the website is not intended to be the primary transaction engine. It exists to show range, demonstrate professionalism, and support in-store trading.

Customers browse online, then switch channels. They call. They email. They visit the shop. Online checkout happens, but it is not the dominant outcome.

In this context, low ecommerce conversion is often a rational result, not a failure. The site is doing its job by driving confidence and contact rather than forcing a transaction.

Problems arise when these retailers judge themselves against conversion benchmarks that do not reflect their operating model.

What repeat visits are really telling you

Across many retailers, sessions per unique visitor sit well above one. Customers are not deciding in a single visit. They are returning to check details, re-evaluate options, and build confidence.

What differs between retailers is not whether customers return, but what they are trying to resolve when they do.

- For destination retailers, return visits tend to reinforce confidence before committing.

- For price-led retailers, return visits often signal hesitation and comparison.

- For store-first retailers, return visits are frequently preparatory, leading to offline action.

Seen this way, conversion rate becomes less about optimisation and more about whether the site resolves the customer’s doubts quickly enough, clearly enough, and credibly enough.

Paid traffic does not create trust, it exposes it

Paid traffic is often treated as a lever that can “fix” ecommerce performance. In practice, it does something simpler.

It increases scrutiny.

Where trust already exists, paid traffic scales outcomes efficiently. Customers recognise the retailer, feel comfortable, and transact.

Where trust is thin, paid traffic brings more people into the evaluation phase without changing the underlying judgement. Conversion remains low, volatility increases, and the gap between traffic and sales becomes more visible.

Paid traffic does not manufacture credibility. It reveals whether customers feel it.

Considered purchases show up clearly in payment behaviour

Two payment behaviours reinforce how trust-led bike ecommerce has become.

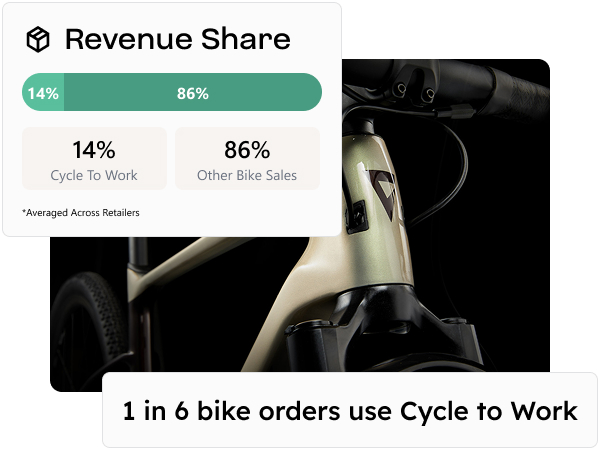

Across this dataset, roughly one in six bike purchases uses Cycle to Work. On Push sites, Cycle to Work is enabled directly in checkout, allowing customers to complete the transaction without back-and-forth contact. Where retailers make this visible and straightforward, it removes friction at the moment the customer has already decided to proceed.

Finance is even more significant. Between a quarter and a third of bike orders use finance, fluctuating by retailer and customer mix. This is not impulse behaviour. Customers are choosing a payment method that spreads cost and risk over time.

Both of these mechanisms increase the number of questions a customer needs answered before committing. They reward retailers who feel established, dependable, and clear. They expose uncertainty where those signals are weak or buried.

The retailers with strong conversion know what problem they are solving

The retailers with consistently strong conversion are rarely trying to make their website do everything.

They are clear on what their ecommerce is meant to do. They understand what their visitors are trying to work out. They know which questions matter most, and they make the answers easy to find without requiring inside knowledge.

Trust signals are not hidden in long paragraphs. They are visible, scannable, and obvious. Customers do not have to work to understand who they are buying from or what happens next.

Where conversion underperforms, it is rarely because effort is missing. It is usually because customers are being asked to infer too much.

A moment of honesty for retailers

At this point, there are really only two productive responses.

One is to sit down and experience your own site as a customer would. Not as the owner. Not with all the context in your head. But as someone arriving cold.

Try to find the product you want. Try to understand who you are buying from. Try to check out. Ask yourself, quickly and honestly:

- Do I immediately trust these people?

- Do I know what happens if something goes wrong?

- Am I reassured, or am I having to think too hard?

- Are the important signals obvious, or buried in walls of text?

Many retailers are surprised by how different the site feels without insider knowledge.

The other option is to talk to people who spend all day looking at this across cycling retail.

A practical sense-check at COREbike

At COREbike, Push will be running private 30-minute ecommerce sessions for retailers who want to sanity-check how their site is being experienced by customers.

These are short, focused conversations led by a team that works exclusively in cycling ecommerce, across retailers of all sizes and trading models. The aim is not to sell a platform, but to help retailers understand which customer-perceived category they currently sit in and whether their site reflects how they actually trade.

Some retailers will leave reassured that their numbers make sense. Others will leave with clarity on why traffic is not turning into confidence.

Details are available at https://go.push.bike/core.

Closing

Customers do not arrive on bike retail websites looking to be impressed by technology. They arrive looking for reassurance.

Conversion rate is where that judgement shows up.

Not as a verdict on effort, but as a signal of whether customers feel confident enough to commit, or whether they are still looking for reasons to trust who they are buying from.

Most experienced operators already feel this instinctively. The data simply shows where that confidence is already doing the work, and where customers are still asking unanswered questions.